What is the difference between a home warranty and equipment breakdown? In this blog I will review the differences and similarities between equipment breakdown insurance coverage and a home warranty.

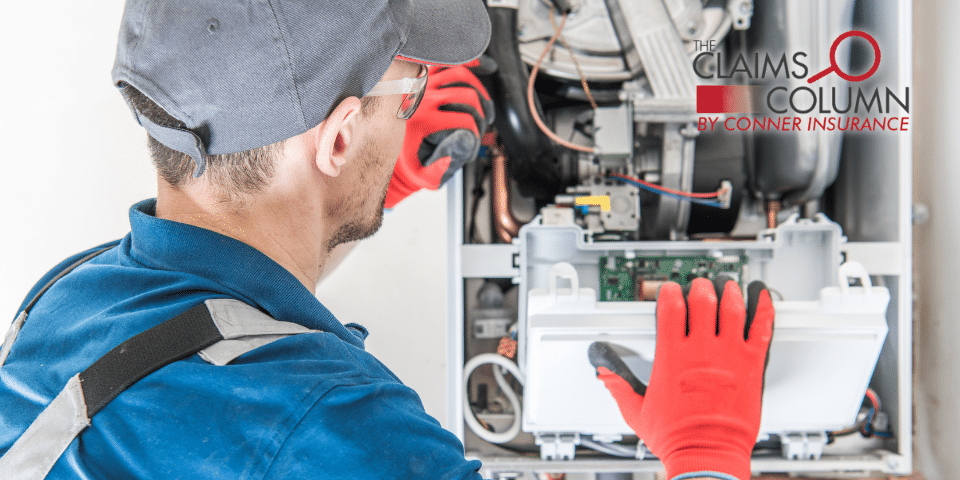

Equipment breakdown coverage is an endorsement that can be added to a homeowners’ policy. There are no square footage limits and coverage is available nationwide. Equipment breakdown coverage losses must be sudden, direct, and accidental. Wear and tear are excluded from equipment breakdown coverage. To get broken equipment fixed, equipment breakdown policyholders can call their own trusted repair vendor to get their equipment fixed.

The home warranty is a standalone service contract. You do not need an existing homeowner’s policy to be eligible for a home warranty. There are square footage limits, and it may not be available in certain states. Home Warranties cover normal wear and tear, however, accidental damage to an appliance or a component is not covered. When an item breaks under a home warranty, the homeowner calls a toll-free number or requests service online. The home warranty company will then assign a local repair professional from their network of approved contractors to come out to the home. It is also important to note that a home warranty can provide general maintenance and home services that most people are looking for, while equipment breakdown is only relevant when the appliances cease to function.

Both equipment breakdown coverage and home warranties cover common appliances and systems that people use in their homes. Some of the appliances that may be covered by both are garbage disposals, washing machines, dryers, refrigerators, ovens, well pumps, water heaters, etc.

We can quote a Home Warranty for you! Please let me know if you have any questions or concerns regarding this matter.

At Conner Insurance, we have set the standard for superior guidance and exceptional service for more than 70 years. Contact us at (317) 808-7711 to speak to one of our advisors. We serve clients across the entire country. Our headquarters is in Indiana and we have satellite offices to serve clients in all 50 states.

Disclaimer: These monthly blogs contain general information and may be subject to change. Policy language may vary by insurance carrier, so please refer to the specific policy in question. The Claims Advocate does not make any representations that coverage does or does not exist for any claim or loss and in no way guarantees coverage for claims.

Funding Is Only the Beginning: Why More Employers Are Exploring Level-Funded Health Plans. When it…

Is a Health Insurance Captive Right for Your Organization? Few employers look forward to renewal…

Back to the Basics: Protecting Your Health Plan from Catastrophic Claims. Part 2. In the…

Back to the Basics: What Your Stop Loss Renewal Can Really Cost. Part 1. When…

Home renovations can be an exciting way to increase your home's value, improve functionality, and…

What Really Drives Reimbursement in High-Cost Claims. When an employee experiences a high-cost claim, the…

{kind=link}