Gas Line Coverage: Insurance vs. Home Warranty

Gas Line Coverage: Insurance vs. Home Warranty. Last week, a client received a letter in the mail from her local gas company, Center Point Energy, offering coverage for gas line repairs. She then reached out to her Account Manager for clarification on what was being offered. After reviewing the entire letter, we were able to explain this offer is essentially a solicitation from an independent company, which is separate from the gas company. The coverage being offered is for interior and exterior repairs to gas lines, but there are low per occurrence limits; $500 per covered repairs for interior restoration and $1,000 per covered repair for exterior restoration.

SERVICE LINE INSURANCE COVERAGE EXPLAINED

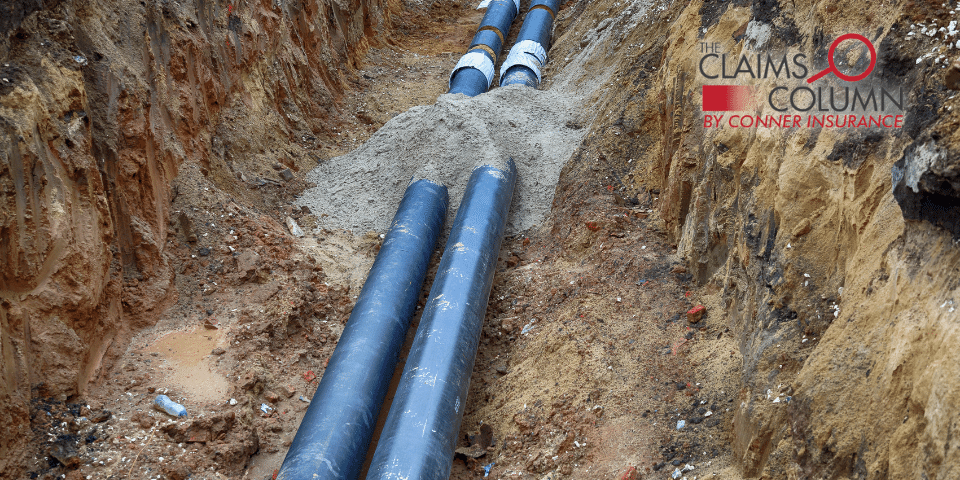

Service line coverage, also known as Buried Utility lines coverage, is an endorsement that can be added to home insurance policies to cover the cost of repairing or replacing a broken utility line. Service lines are the underground utilities running into the home, that connect the home to the city’s main supply for utility services. The homeowner is responsible for these lines in the event of degradation, damage, or breakdown. Service lines include water pipes, power lines, cables/fiber optics and the main sewer line that runs from the home to the street. For most carriers, the following damage is NOT covered under service line: underground wires or pipes that are not connected and ready for use, fuel tanks, heating/cooling systems, septic systems, sprinkler systems or lines going to outdoor pools, pollutant clean up, and wiring or piping that runs through water. To learn more about service line coverage, read one of our latest blogs.

HOME WARRANTY GAS LINE COVERAGE EXPLAINED

The coverage with the independent company that sent the letter to our client differs from Service Line because it does offer coverage for interior gas lines. As mentioned in the letter, a typical HO policy will not cover wear and tear/maintenance issues. If there is Service Line coverage on the policy, then the primary exposure for the homeowner is potential damage to interior line and if they feel the coverage is beneficial, I recommend contacting the company directly for questions or concerns and reviewing the policy in its entirety. I was also able to obtain a copy of the policy offered by the independent home warranty company which is available at their website. In my opinion, the coverage doesn’t make good financial sense because essentially the client is paying $8-22 a month for very low per occurrence limits, but of course the final decision is up to the client.

CONTACT

At Conner Insurance, we have set the standard for superior guidance and exceptional service for more than 70 years. Contact us at (317) 808-7711 to speak to one of our advisors. We serve clients across the entire country. Our headquarters is in Indiana and we have satellite offices to serve clients in all 50 states.

Disclaimer: These monthly blogs contain general information and may be subject to change. Policy language may vary by insurance carrier, so please refer to the specific policy in question. The Claims Advocate does not make any representations that coverage does or does not exist for any claim or loss and in no way guarantees coverage for claims.